|

| Private Gold Reserves - India (2ndlook model) |

Quiet Progress

For the last 20 years, World Gold Council has shown Indian gold consumption rising from 400 tons (1987) tons to 800 tons (2007). Estimated Indian gold reserves at 25,000-30,000 are double of the next largest country - the USA with 14,000 tons. India has 20% of the world population and also 20% of the world’s above-the-ground gold.

Which is quite unlike China!

India and the World

For much of the last 2000 years of recorded history, India has been the largest buyer of gold. Roman historian, Pliny, lamented some 1800 years ago, how India, the sink of precious metals, was draining Rome of gold - an appellation that resonates even today.

In the Indian North West (modern Afghanistan), Greco-Bactrian coins were made (seemingly) from the “Roman gold coins, which poured into India.” To “manage” this drain of gold, Romans started cheating the Indians. They reduced the gold content in coins. Septimus Severus, (193 AD-211) further debased the currency. Indians just stopped accepting the debased coin - and demanded payment in pure gold.

In mid 17th century, a Superior of the Capuchin Mission at Isfahan, friar Raphael du Mans wrote an authoritative (in 1660) Estat de la Perse, which was used by the French MinisterJean Baptiste Colbert, to form the French East India company (1664) - and in modern times, as a source book for tobacco habits in medieval Iran. This Christian missionary in Iran, Raphael du Mans thought that India is “where all the money in the Universe is unloaded as if into an abyss.” Central Asian invaders, for gold, aimed at the सोने कि चिडिया (loosely the ‘golden goose’). Their partially successful raids, were deemed as invasions by colonial historians.

The Byzantine Empire, successor to the Assyrian-Achmaenid-Macedonian-Roman lineage, similarly found that their reserves of precious metals were ‘again, leaked away to India.’ A significant part of Indian royal treasuries, when these hoards “fell a prey to European invaders, it was found that the gold coins of the Byzantine emperors formed no small part of their treasures”

In 1748, Baron de Montesquieu, warned Europeans that …

Every nation, that ever traded to the Indies, has constantly carried bullion, and brought merchandises in return. … commerce of the Romans to the Indies was very considerable … this commerce was carried on entirely with bullion … They want, therefore, nothing but our bullion, to serve as the medium of value, and for this they give us merchandises in return … that bullion was always carried to the Indies, and never any brought from thence. (ellipsis mine).

Restrictions on export of gold from Iran to India to India were put by the Safavid Iran. - and the Ottomans in turn put restrictions of export gold to Iran. No help at all.

Even modern writers resent the fact that despite the “absence of indigenous sources of gold and silver” the “very favourable export-import balance” resulted in “inherent strenghth of the Indian economy”. Further, it has been correctly observed that in “our period the subcontinent drew vast amounts of gold and silver, exceeding previous periods and exceeding all other parts of the contemporary world so far.”

A French visitor to India Francois Bernier enviously wrote how

It should not escape notice that gold and silver, after circulating in every other quarter of the globe, come at length to be absorbed in Hindostan. (from Travels in the Mogul Empire By François Bernier, Irving Brock)

Another current day writer describes how

“in exchange for textiles, spices and other Indian agricultural and industrial products, merchants from across Europe and Asia flooded India’s bazaar’s with dinars, tangas, ducats, guilders, reals, francs, rixdollars (reichthalers) and countless other varieties of coins, all of which were minted into rupees. (from The Indian diaspora in Central Asia and its trade, 1550-1900 By Scott Cameron Levi)

Moving away from Central Asia, the general European economy, was simple -

Europe had a net balance in the difference between the arrivals of precious metals (mostly from the New World after the sixteenth century) and export of the same (mostly to the Far East for the purchase of luxury commodities).(from Economic systems and state finance By Richard Bonney, European Science Foundation)

It was not surprising therefore to find that Ian Fleming, pitted Western fiction’s best secret agent, James Bond against Auric Goldfinger - who was smuggling gold out of a declining, post-war Britain to India.

And Indian exports were not only textiles, spices and indigo. Students came from all over the world - and paid large sums of money to Indian teachers for education!

The Pre-WW2 Currency Crisis

During various collapses of temporary gold standards in history, Indian gold reserves (usually unwillingly) stabilised world economies. In recent history, Indian gold reserves went out to stabilise the American currency during the Great Depression and the German currency during the post-Wiemar drift. Indian silver reserves broke the Hunt Brothers’ back and their silver gambit in the 1980’s.

After (colonial) India’s accession to the world gold standard in 1898, India, especially during WW1, rapidly built up a export surplus. British reserves of gold started drying up - in spite of gold export restrictions to India by the USA, Britain and much of the Western world. There was hysteria in popular press and politicians on the subject of India and its appetite for gold.

Crash in silver prices

Between 1800-1900, new mines and increased silver production saw a crash in silver prices. Abundant silver discoveries and mining had flooded the world with silver, depressing prices. Germany moved to the gold standard in 1873, further releasing silver in the world markets. The Opium trade further released vast amounts of silver from China - which was opened to ‘free trade’, giving rise to some of the biggest Western fortunes (of the Roosevelts, for instance).

US silver coinage was being depreciated due to increasing supplies of silver.

On the other side, Britain had a large debt due to WW1 - principally to the US of A and India. Groaning under the weight of WW1 debt, Britain took the easy way out to assuage the impatient creditor - US of A. Britain and America stuck a deal at the cost of the Indian subjects of the British Raj. They paid the US in gold - sourced from South Africa, Ghana, Australia and Canada - and instead bought silver from the US at inflated prices, to settle Indian debts.

Britain decided to settle Indian debts with silver. Large US silver reserves were released when the US passed the Pittman Act which mandated silver sales at more than a dollar per ounce - double the 50c per ounce prevailing price of silver. The resulting payment crisis was averted, and it was decided to pay India in silver released by the Pittman Act. Silver prices which were ruling at o.50p an ounce in the London market, was sold to the Indian colonial Government for more than US$1.0 under the Pittman Act.

Gold prices were deflated. Interest rates in India were increased. Restrictions on gold (and even silver) imports on were placed and gold demand in India was ‘normalized’. Subsequently, even payments in silver became difficult. India then started getting paid by Bank Of England credit notes.

So, finally, it was the Indian native who financed the WW1, who paid the price!

But of course, the Indian native was ungrateful to the US of A who, “by passing the Pittman Act, Congress gave India an opportunity to obtain silver” (from Our silver saved India from crisis - New York Times, Published, August 23, 1918).

Modern restrictions on gold exports to India

Between WW1 end and the start of the WW2, it was evident that sooner rather than later, India would not remain a colony for long. Between 1920-40, in a series of measures, policy decisions were taken, which made Indian interests subsidiary and inferior to Western interests. Central bankers from the USA, Britain, France and Germany had many meetings “coordinate monetary policy.” The agenda - gold flow management between themselves and an obvious understanding - don’t let the browns get the gold.

Indians were paid, with inflated and abundant silver stock, instead of gold. This silver was the same silver released by the Pittman Act. The silver buffer solution to the gold drain to India was seen as the “only buffer to protect Western gold reserves against the Indian drain (was) a silver buffer.” Of course, later the British Raj decided to settle Indian debts with promissory notes - and not even silver. It was this Indian ‘sacrifice’ which enabled the recovery of the West.

They (Hjalmar Schacht, Governor, Reichsbank, Charles Rist, Deputy Governor, Banque de France, Benjamin Strong, USA Federal Reserve, Montagu Norman, Bank Of England) agreed that Indian demand for gold had a “…deflationary effect on global liquidity,” therefore Indian demand for gold had to be regulated.”

in the spring of 1926, when Norman induced Strong to support him in fiercely opposing a plan of Sir Basil Blackett’s to establish a full gold-coin standard in India. Strong went to the length of traveling to England to testify against the measure, and was backed up by Andrew Mellon and aided by economists Professor Oliver M.W. Sprague of Harvard, Jacob Hollander of Johns Hopkins, and W. Randolph Burgess and Robert Warren of the New York Reserve Bank. The American experts warned that the ensuing gold drain to India would cause deflation in other countries (i.e., reveal their existing over-inflation) (from America’s Great Depression By Murray N. Rothbard, Chapter 5, The Development of the Inflation; Ludwig von Mises Institute)

The Anglo Saxon bloc clearly realized that “it was most important for the Allies to agree on a policy that would prevent the Huns from capturing the very valuable raw materials which can be obtained in India, and sometimes in India alone” (from Our silver saved India from crisis - New York Times, Published, August 23, 1918). Further, The New York Times stated “how without Indian products there would be greater difficulty in winning the war” (from SELLING OUR SILVER TO INDIA from The New York Times, Published - August 25, 1918).

So, as the West traded, profited and consumed Indian production and goods, when it came to paying for the goods, they cavilled - and ‘regulated’ Indian demand for gold - and even silver!!

How millions of Indians died

Like much of Western history, the British Colonial administration (Lord Willingdon, Montagu Norman, Neville Chamberlain, Winston Churchill, the Chancellor of the Exchequer) executed a scorched earth policy in India. (After all what is brown life worth?)

They implemented a series of economic and administrative measures, (significantly, under Churchill’s baleful influence) that killed millions in the Bengal Famine would impoverish India - and sustain the empire. The result - Bengal Famine of 1943 which killed 40 lakh Indians. The Bengal Famine of 1943, of course had may other layers to it - but nett, nett, as Gideon Polya has pointed out, Australian sheep have lower mortality rates.

The Bengal-Burma link of the ages was broken. After being demonized, the Chettiar money lenders were thrown out of Burma, the role of Chettiars (for e.g. in Singapore) was wiped clean. From being a granary of Asia, Burma started declining - and there was no rice for exports. Result - The Bengal Famine of 1943. Tally - 40-50 lakh deaths.

|

| Cabinet ministers, August 1931. Back row (left to right): C Lister, J Thomas, Rufus Isaacs, (Lord Reading), Neville Chamberlain and S Hoare (Viscount Templewood). Front row (left to right): Philip Snowdon, Stanley Baldwin, prime minister Ramsay MacDonald, H Samuel and Lord Stanley. Photograph -Courtesy Guardin, UK, Source: Getty Images |

After the fall of Singapore, and the rapid Japanese advance, with Subhash Chandra Bose in the vicinity, a revolt by Bengal would have had catastrophic effect on the colonial administration. Howard Fast, in his novel ‘The Pledge’ believes that the Bengal Famine was deliberate creation - possibly to weaken the local population and deter support for Subhash Chandra Bose.

Crisis in Britain

Britain in the meantime, returned to the gold standard under Montagu Norman and Winston Churchill (then the Chancellor of the Exchequer) - with the famous prediction by Keynes that this action would result in a world wide recession - of which much came to pass. Churchill confessed “I’m lost and reduced to groping” but went along with Montagu Norman, united by their racism.

On October 27th, 1931, the Ramsey Macdonald led “National” Government (Conservatives and Liberals coalition, fearful of the rising Labour Party) in Britain won a huge majority of 554 MPs of 615. The economic crisis of September (misnamed as the Indian Currency Crisis), ensuing Depression era problems in the US, the Weimar Republic problems - and other issues pushed this ‘National’ government to ram through a series of measures (page 130-131) that depressed silver prices, inflated gold prices and raised interest rates in India.

Done over the protests by Gandhiji, trade bodies and merchants and threats of resignation by the Viceroy and his Executive Council, the resulting ‘money famine’ (page 155) had the Lord Willingdon ecstatically say ‘Indians are disgorging gold.’ Indians have a different reason to revile Neville Chamberlain, who with great satisfaction said “…The astonishing gold mine that we have discovered in India’s hordes has put us in clover …” after impoverishment of the Indian serf. |

| More currency, less gold. Drawing courtesy - imf.org |

The Nixon Chop

On August 15th, 1971, President Nixon after a two day huddle with 15 advisers at Camp David, delivered the Nixon Chop to the world.

The Nixon chop (my name for this event), one month after his China breakthrough, cut the convertibility peg of US$35 to gold as US gold reserves were severely depleted. The French had been regularly redeeming gold for their dollar earnings - and for this ‘perfidy’ the US had not forgiven France. This was much like the pre-WW2 French methodology of devaluation, new peg, old debt for new gold routine which got the US hackles up. Many decades have passed since these redemptions by France, and the new French President, Sarkozy believes it is now possible to renew US-French relations again.

On the opposite side of the world, a beleaguered Indian Prime Minister was celebrating 24 years of Independence with a “ship-to-mouth“ economy, dependent on PL-480 grain. Private gold reserves in the Indian economy after nearly 25 years of post-colonial rule, were steadily rising. Over the next 10 years, the Western world (and most of the rest) blamed OPEC for post-1971 inflation, gold scaled US$800 an ounce; the Hunt Brothers launched their bid to corner the silver market; stagflation made an entry and Soviet power grew. Nixon Chop, itself the result of many years of gold reserves erosion, was one in many steps that brought the US$ to its knees - only to be saved by the Oil dollar tango.

The Greatest Crime Wave … Ever?

From the 1960-1990, the Big Issue for people across large parts of the world was Big Crime. The 1960-1990 peak in organized crime, globally, is interesting due to the synchronized time frames - across USA, Europe and India.

In India, the rise of the underworld was delayed by a decade - as was its decline. India’s underworld, centred in Mumbai, at its peak, intruded into trade unions, films and entertainment, gambling, real estate, extortion and smuggling. The specter of Dawood Ibrahim haunts India-Pakistan Governmental relations - even today.

Roosevelt had earlier in 1933, during his New Deal years, nationalized all American gold. This restriction was finally eased only on December 31st, 1974, with Executive Order 11825 by Gerald Ford. It was Roosevelt’s gold nationalization which allowed the US to wage WW2 and create the Bretton Woods system.

From 1939, (the start of WW2), gold imports into India, the world’s largest market and also the largest private reserve of gold, were controlled or banned. Not only the largest, but Indian reserves of gold, are also the only significant reserve in the world without a history of war, genocide, slavery or loot, (unlike US, UK, Canada, Australia) or to due nature’s bounty (unlike South Africa, China, Peru, Ghana, etc.).

The first effect of restrictions on gold imports in India was on prices. Indian gold prices, on an average, were 30%-40% higher than international prices. The other thing that happened was that gold imports went underground. Gold imports (illegal), called smuggling, spawned the biggest criminals that India has seen.

The common threads in this were, of course, America, drugs, underworld, war, corruption, warlords - but what made all this possible was Indian appetite for gold.

All this was made possible by the Indian hawala system of money exchange. Hawala made money transfers safe, instantaneous, at a low cost. Traditional Indian ships from a thousand ports in Goa, Maharashtra and Gujarat sailed with this contraband and brought back gold.

|

| Drug production centres surround India - Golden Triangle & Golden Crescent |

The countries comprising these Golden Triangle /Crescent are India’s neighbours. The Indian underworld transported drugs through India. These drug shipments originated, were acquired, grown and traded from the Golden Crescent and the Golden Triangle.

The US eliminated gold ownership restrictions in 1975. India followed. In 1992, India started its first hesitant steps towards legalizing gold imports. By 1995, these import control laws had been diluted to near non-existence. With the dilution of restrictions on gold imports came the abatement in the biggest crime wave in modern history.

Today, the abatement in organized crime is ascribed to vigourous efforts by the police and legal systems. The earlier lack of success is conveniently forgotten. Many ‘encounter’ specialists claimed credit for the reduction in the power of the India’s underworld. Much like the fading away of the mafia in the US and Italy, in India too, after the gold trade was legalized, the mafia’s source of power, liquidity, earnings, profit were taken away. With it came the underworld’s loss of power and influence. And that coincided with the reduction and control of organized crime from the US and Europe and India. And an end to the greatest crime wave in the modern history

|

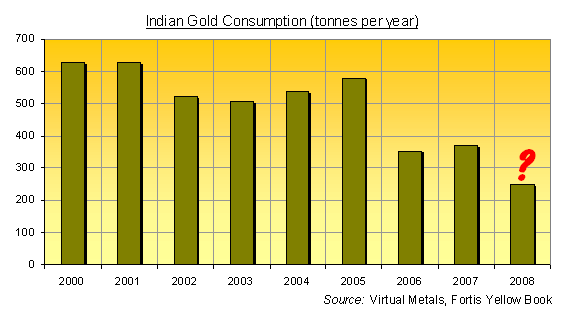

| Indian gold consumption (Click for larger image.). |

So, why this desperate poverty

With global monetary system in a flux and the decline of the dollar (especially after the Plaza Accord), the perceived utility of gold and the price outlook of gold has been positive. After the Nixon chop, at an estimated 15,000-18,000 tons, India was in a position to create instruments, obtain leverage and create wealth from the world’s largest gold reserves.

It is the failure of the Indian economic minds - that they have not found any instruments and means. Some 35 years after the Nixon Chop, and with Indian gold reserves approaching 30,000 tons mark. Some other countries tried feebly, and failed. Japan and Asean tried setting up the Asian Monetary Fund - after 1997, currency crisis - and were arm twisted by the US to drop the idea.

Is the US likely to give up the central role?

Unlikely! Let me correct myself! Pretty damn unlikely!!

Will the Western world share its pre-eminence with Japan, China and India. Bet your bottom yuan, yen, rupee or gold - they wont. Especially since the Anglo Saxon Bloc control nearly 80% of world gold production.

What are they likely to do! Some of the older measures by which gold was transferred from the old (and the new) world to Western world are no longer possible.

But if any central bank (or monetary authority) were to: -

- Mask purchases

- Build up gold positions

- Take physical possession of gold (Avoid Czech Gold, Montagu Norman & BIS Scam)

- Look at a positive outcome to a war scenario

then that country will be able to bolster their gold reserves position by: -

- About 10,000-15,000 tons

- Limit the cost of purchase

- Make it economically unviable for anyone else to match them

The only country that can (currently) match these criteria is the USA - and China.

The US GATA Committee has been running a low profile campaign on gold price manipulation. This attempt, if successful, at increasing gold prices will possibly make it difficult for Indians to buy gold in larger quantities. The Indian Central Bank, preoccupied with a developmental agenda, is in no position to take up this challenge.

From an Indian standpoint

While the silver lining is private reserves, we have a blinkered RBI & GOI response. India has one of the lowest monetary reserves of gold in the world. Against a global average of 10.5% RBI holds only 3.4% of its reserves as gold. The EU holds 40% of its reserves in gold and USA - 70%.

And while the RBI & GOI gently sleep, the Chinese have grown their gold purchases. China has become world’s 3rd largest consumer of gold - up from a 100 tons to 350 tons. Shanghai Gold Exchange has made it easier for individuals to invest in gold by reducing the transaction size from 1 kg to 100 gm.

Importantly: -

- Is India in a position to militarily defend these reserves

- Does the GOI and the RBI have any strategic intent vis-a-vis gold

Making the job easier for the GOI and the RBI are Indian economic habits of the centuries that have allowed this build up of gold reserves. India stands at a historical cross road. Are Indian economic and political minds at work to exploit this window of opportunity. Or will it be a wasted chance.

Gold and War

Alexander’s campaign started with the gold reserves that his father had built from the mining operations at Mount Pangeus. The Macedonians were the first in the Hellenistic world to keep standing army - a luxury and a big expense, in Greece, at that time. The Roman empire was similarly funded by gold mining and loot. Julius Caesar’s European conquests were funded by Gaellic loot. The Punic Wars with Carthage were fought over Spanish Gold. Roman conquest and love affair with Egypt was motivated by grain and Nubian gold.

Carolus Magnus, Karel de Grote, Karl der Grosse, Carlomagno, Charles the Great - or more commonly known as Charlemagne (ruled between 768-814) waged war for 30 years, spread over more than 50 battles. Charlemagne’s conquests were funded by the Saxony mines, the Haartz mountains, etc. His victory over Avars, (modern Hungary) gave him treasures which needed 15 carts, pulled by grey steppe oxen for transport.

The British loot from Canada, Australia, South Africa - and India, gave the world, numerous wars and brought humanity “under the heel by means that will not bear scrutiny.” It is these very same Gold reserves which gave birth to the Bretton Woods - and we know what happened after that! Roosevelt gave a New Deal to the Americans. He took away all their gold. WW2 followed soon thereafter.

This short look at Western history makes the linkage between the pattern of gold ownership and war becomes clear.

|

| Regional gold holdings |

What Should We Do With Gold

Just sell it to people. From all the countries of the world.

The world financial organization should limit control of global gold output by any mining organization to 10% or a single mine - which ever is lower. Gold holding should be widely dispersed, as widely as possible, amongst individuals - like the Indian gold possession model. No national government, in the new financial architecture should not be allowed to have more than 250 tons of gold - to progressively reduce to 50 tons.

What this will do is disperse gold holdings among the citizens of the world - and dilute the ability of nations to wage war! National Governments (like the US), have used gold looted from their own citizens (and others) to deprive other peoples of the world of gold - and wage war.

What we should not do?

Good Ole’ Gold Standard

In the last few decades between the Nixon Chop and the Bush Whack, the Western academic world, has floated another ‘hot air’ balloon. It is the revival of the ‘pure,’ Gold Standard. The story goes that in the ‘olden’ days of 19th century, in the golden age of Western civilization, there once reigned the Gold Standard.

The simplistic logic of this theory is that the world should ‘go back’ to the Gold Standard - or as some put it, improve the ‘corrupted Gold Standard’ of the 19th century, and then everything will be fine. All currencies of the World, should be indexed to Gold - and then everything should be fine. Currency can be redeemed against gold - and gold reserves equivalent to currency should be kept as reserves. This will kill inflation, stop war, make politicians honest, make tax payers honest, citizens hard working and business efficient.

In short a magic bullet.

The last time, we saw this, it was called the Bretton Woods. The US and the Anglo Saxon Bloc came together and said we will administer the new world currency system. The world agreed - once again. And we know what happened.

Two years ago …

This post had estimated that the Chinese could possibly (and they have) increase their monetary gold reserves. On April 24th, 2009, Bloomberg reported that China had increased

its (gold) reserves by 454 tons to 1,054 tons through domestic purchases and refining scrap metal, Hu Xiaolian, head of the State Administration of Foreign Exchange, said in an interview with the Xinhua News Agency today. China, the world’s biggest gold producer, has increased its holdings before, Hu said in the interview carried on the administration Web Site. They rose from 394 tons to 500 tons in 2001 and to 600 tons in 2003. The U.S. has the world’s biggest gold holdings at 8,134 tons, followed by Germany with 3,413 tons, World Gold Council data show. France has 2,487 tons and Italy 2,452 tons, while the IMF has 3,217 tons, according to the council.

Another report, from Market Watch, a WSJ web publication added,

The increase makes China the world’s fifth-largest holder of gold, just ahead of Switzerland, and among the six nations plus the International Monetary Fund that have reserves of more than 1,000 metric tons. Although Hu did not elaborate on where China had sourced the additional bullion, her comments were interpreted as meaning they came from domestic sources and may included refining of scrap metal. Traders also say the gold was accumulated systematically over a number of years. Last year China ranked as the world’s largest gold producer with 12.2% of world output, equivalent to 288 metric tons. The U.S. ranked second with a 9.9% share, or 234 metric tons.

What are the future plans of the Chinese? A report quotes an analyst

China should increase its gold reserve from 600 tons to about 2,500 tons in a short term and to 3,000 tons in a long term to cope with the versatile exchange rate risks, said Teng Tai, an economist of China Galaxy Securities Company.

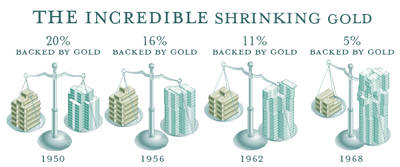

Of course, this really does not mean much - except that it may keep gold prices on boil. Whether a currency is backed by a 5% or a 10% gold reserve may not mean much, in this era of rampant use of (not just by the US of A) “a technology, called a printing press” as an economic tool. For long term economic stability, gold needs to be in the hands of individuals - and not Governments.

No comments:

Post a Comment